What information are you looking for?

Sentences as well as single words are supported. Queries and answers supported in over 60 languages.

The content of the questions asked will not be saved or used for AI learning purposes.

Corporate members may use the service free of charge.

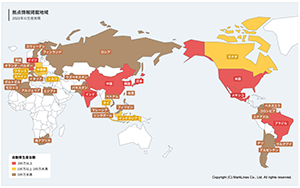

Japan

Japan USA

USA Mexico

Mexico Germany

Germany China (Shanghai)

China (Shanghai) Thailand

Thailand India

India